If you’re running a business in Phoenix and your accountant hands you a Profit & Loss statement, your first instinct might be to nod politely and file it away without really understanding what you’re looking at. You’re not alone. Most small business owners in the Valley are experts in their craft — whether that’s construction, consulting, retail, or services — but financial statements weren’t part of the job description when they started. The problem is that your P&L is one of the most powerful tools available to you as a business owner, and not understanding it means making decisions with incomplete information.

A Profit & Loss statement — also called an income statement or P&L — is a financial report that shows how much revenue your business brought in, what it cost to generate that revenue, and what was left over as profit or loss over a defined period of time. It doesn’t show your bank balance or what you own and owe — that’s the balance sheet’s job. What the P&L shows is performance: specifically, whether your business is actually making money and where that money is going. Reading one doesn’t require an accounting degree. It requires understanding about eight key numbers and what each one is telling you about your business.

Why Your P&L Matters More Than Your Bank Balance

Most Phoenix business owners manage their finances by watching their bank account. Money comes in, money goes out, and as long as the balance stays positive, things feel okay. This approach is understandable but dangerously incomplete. Your bank balance reflects cash timing — when invoices were paid, when checks cleared, and when you ran payroll. It does not tell you whether your business model is actually profitable.

You can have a healthy bank balance while your business is quietly losing money. This happens all the time with seasonal businesses, businesses that invoice in advance, and companies that took on debt to fund operations. Conversely, a profitable business can have a tight bank balance during a growth phase when it’s investing in inventory, equipment, or staffing. The P&L cuts through the noise of cash timing and shows you the actual economic performance of your business — revenue earned versus expenses incurred, regardless of exactly when cash changed hands.

For Phoenix business owners specifically, understanding your P&L becomes even more critical during tax season. Arizona Tax Accounting and Consulting Services uses your P&L as one of the primary documents for calculating your tax liability, identifying deductions, and planning ahead. When your P&L is accurate, and you know how to read it, those conversations with your accountant become far more productive — and far less stressful.

The Structure of a Profit & Loss Statement

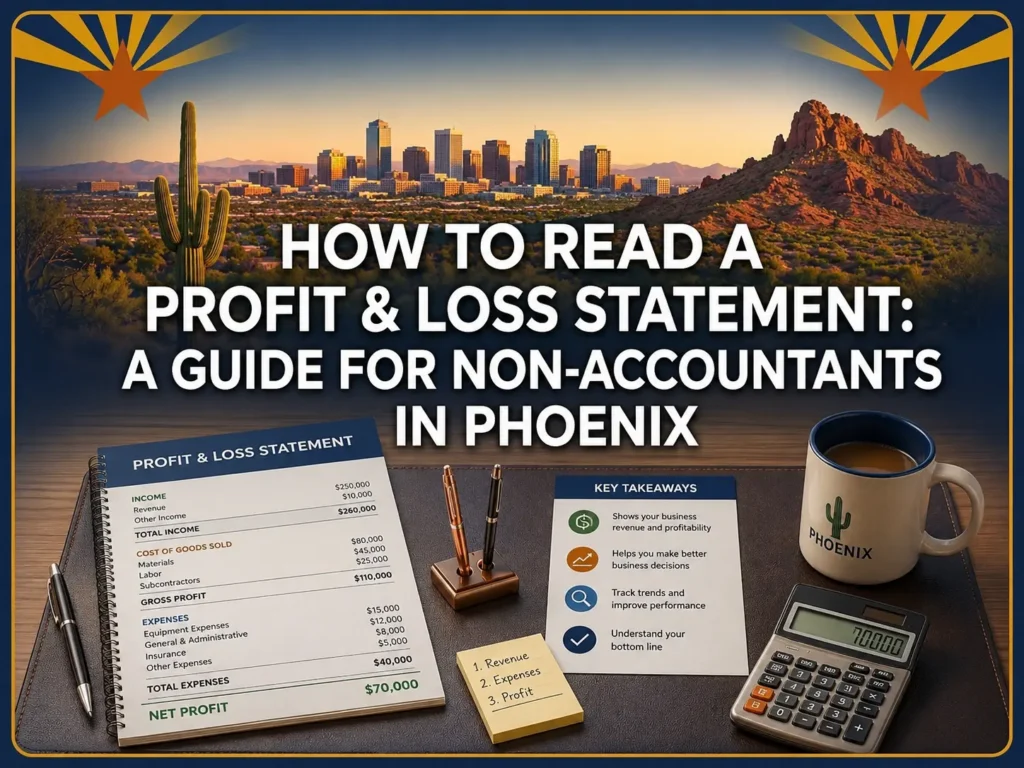

Every P&L follows the same logical flow from top to bottom. Revenue sits at the top. Expenses are deducted in layers below it. What remains at the bottom is your net profit or net loss — often called the “bottom line.” Each layer between the top and bottom represents a different level of profitability that tells a slightly different story about your business. Here’s how to read each one.

Revenue: The Starting Point

Revenue — sometimes labeled “Sales,” “Income,” or “Gross Revenue” — is the total dollar value of everything your business sold or billed during the period covered by the statement. It’s the first number at the top of the P&L, and it represents money earned before any expenses are considered.

For most Phoenix small businesses, revenue is straightforward: it’s your total invoiced sales or receipts for the month, quarter, or year. However, if your business issues refunds, provides discounts, or has returns, those reductions are typically subtracted from gross revenue to arrive at net revenue — the amount the business actually kept from sales activity. This distinction matters because gross revenue can look impressive while net revenue — after refunds and discounts — tells a more accurate story of what the business actually collected.

One important nuance for business owners new to accrual-based accounting: revenue on a P&L is recorded when it is earned, not necessarily when it is received in cash. If you completed a job in December and invoiced the client, that revenue shows up in December’s P&L even if the client doesn’t pay until January. This is standard accrual accounting and is how most professionally prepared financial statements are structured. It’s also why your P&L profit and your bank balance don’t always match — and why both numbers matter.

Cost of Goods Sold: What It Costs to Deliver Your Product or Service

Directly below revenue on the P&L is the Cost of Goods Sold, commonly abbreviated as COGS. This section captures the direct costs of producing or delivering whatever your business sells. For a Phoenix construction company, COGS includes materials, subcontractor labor, and direct job costs. For a restaurant, it’s food and beverage costs. For a service business, it might be the cost of the labor hours directly spent delivering the service.

What COGS does not include are the background costs of running the business — rent, utilities, office salaries, marketing, and insurance. Those are operating expenses and appear lower on the statement. COGS is strictly the cost directly tied to producing your revenue.

Understanding your COGS is important because it determines your gross profit, and your gross profit margin is one of the first indicators of whether your pricing and production efficiency are working. A Phoenix business with $500,000 in revenue and $350,000 in COGS has a gross profit of $150,000 and a gross margin of 30%. Whether that’s healthy depends entirely on the industry. A construction contractor might target 20–30% gross margins, while a software company might aim for 70–80%. Knowing your gross margin and how it trends over time is one of the most revealing things your P&L can tell you.

Gross Profit: Your First Profitability Signal

Gross profit is simply revenue minus COGS. It represents the money left over after covering the direct costs of your products or services — before paying for the overhead of running the business. The formula is straightforward:

Gross Profit = Revenue − Cost of Goods Sold

Gross profit tells you whether your core business activity is profitable at the transaction level. If your gross profit is thin or negative, you have a fundamental pricing or cost problem that no amount of expense reduction in other areas will fix. If your gross profit is healthy, it means you have margin to work with, and the question becomes whether your operating expenses are sized appropriately relative to that margin.

Tracking gross profit over time is also one of the most effective ways to catch problems early. If your revenue is growing but gross profit margin is shrinking, it often signals rising material costs, scope creep on projects, inefficient labor use, or pricing that hasn’t kept pace with cost increases — all issues that are far easier to fix when caught early than when they’ve been quietly compressing margins for 12 months without anyone noticing.

Operating Expenses: The Cost of Running the Business

Operating expenses — sometimes broken out under labels like “General and Administrative Expenses,” “Overhead,” or “Selling, General & Administrative (SG&A)” — represent the costs of running the business that are not directly tied to producing your product or service. These are the fixed and semi-fixed costs that exist whether you make one sale or a hundred.

Common operating expenses for Phoenix small businesses include:

- Rent or mortgage on office or commercial space

- Utilities, phone, and internet

- Employee salaries and wages for non-production staff

- Payroll taxes and employee benefits

- Marketing, advertising, and website costs

- Professional fees — accounting, legal, consulting

- Insurance premiums

- Vehicle expenses and mileage reimbursements

- Depreciation on equipment and assets

- Software subscriptions and office supplies

The detail of operating expenses in your P&L is where most business owners find the most actionable information. Reviewing operating expenses line by line each month reveals spending patterns, identifies categories that are growing faster than revenue, and highlights costs that may have been set up on autopay and forgotten. A $300 monthly software subscription that nobody on your team uses anymore adds up to $3,600 per year in unnecessary expense — and that kind of quiet cost creep is extremely common in small businesses.

Operating Income: Profitability From Your Core Business

Operating income — sometimes called operating profit or “income from operations” — is calculated by subtracting total operating expenses from gross profit. This number tells you how much your business is making purely from its core operations, before accounting for interest on loans, taxes, and non-recurring items.

Operating Income = Gross Profit − Operating Expenses

Operating income is particularly useful for evaluating whether the business model itself is working, independent of financing decisions and tax obligations. Two Phoenix businesses might have very different net profits simply because one carries significant debt and the other doesn’t — but their operating income would reveal whether both are actually running efficient operations. If your operating income is positive and healthy, your business is generating value. If it’s negative, the business is consuming resources faster than it’s generating them, and addressing that requires looking at either the revenue side, the cost structure, or both.

Below the Operating Line: Interest, Taxes, and Net Profit

Below operating income, the P&L accounts for the remaining items before arriving at the final bottom line:

Other Income and Expenses — These are items outside of normal business operations, such as interest income on a bank account, gains or losses from selling an asset, or one-time settlement payments. These items are separated from operating income because they don’t reflect the ongoing performance of the business.

Interest Expense — If your business carries debt — a business line of credit, SBA loan, equipment financing, or commercial real estate mortgage — the interest paid on that debt appears here. It’s an expense that reduces profitability but is separate from operating expenses because it reflects a financing decision rather than an operational one.

Income Tax Expense — For business entities that carry tax liability at the entity level, income tax appears as a line item here. Pass-through entities like LLCs and S-Corps typically don’t show income tax at the business level because the tax flows to the owner’s personal return, but C-Corporations and some entities do carry this line.

Net Profit (or Net Loss) — This is the true bottom line: what remains after every expense, interest payment, and tax obligation has been accounted for. Net profit is the number that reflects whether the business is building value or eroding it.

Net Profit = Operating Income + Other Income − Interest Expense − Income Tax

Key Ratios That Give the P&L Deeper Meaning

Reading the raw numbers on your P&L tells you what happened. Calculating a few simple ratios tells you how well your business performed and gives you benchmarks to track over time.

Gross Profit Margin = Gross Profit ÷ Revenue × 100

This percentage tells you how much of every revenue dollar remains after covering direct costs. If your gross margin is 35%, you keep $0.35 from every dollar of sales to cover overhead and profit.

Operating Profit Margin = Operating Income ÷ Revenue × 100

This shows how efficiently the business converts revenue into operating profit after all overhead is accounted for. Industry benchmarks vary widely, but tracking this number month over month reveals whether operational efficiency is improving or declining.

Net Profit Margin = Net Profit ÷ Revenue × 100

This is the ultimate measure of overall profitability — the percentage of revenue that becomes actual profit after everything is paid. For many Phoenix small businesses, a healthy net margin sits somewhere between 8% and 15%, though this varies significantly by industry.

Calculating these three margins and comparing them to prior periods is one of the most straightforward ways to use your P&L proactively rather than just treating it as a backward-looking record.

Common Mistakes Phoenix Business Owners Make When Reading Their P&L

Understanding the structure of a P&L is only part of the picture. Knowing how to avoid the most common misinterpretations is equally important.

The most frequent mistake is treating net profit as available cash. Profit is an accounting concept — it reflects revenue earned minus expenses incurred during the period. It does not tell you how much cash is sitting in your bank account. Loan repayments reduce cash but don’t show up as expenses on the P&L. Purchasing equipment reduces cash but may be capitalized as an asset rather than expensed. Conversely, depreciation is an expense on the P&L that doesn’t reduce cash at all. This is why cash flow management and P&L analysis work together but serve different purposes.

Another common mistake is reviewing the P&L only once per year — typically when it’s handed over to an accountant for tax preparation. By that point, the information is 12 months old and the window for acting on what it reveals has largely closed. Monthly P&L review is the standard recommended by every experienced CPA because it gives you the ability to spot and correct problems within the same quarter they develop, not 12 months later.

Finally, many business owners focus exclusively on net profit without reviewing the layers above it. A business can have a strong net profit in a given month because of a one-time gain while operating income is actually declining. Looking only at the bottom line misses that signal. Reading the P&L from top to bottom and understanding what each layer is saying gives you a far more complete picture of your business’s health.

How to Use Your P&L for Better Business Decisions

Once you’re comfortable reading your P&L, it becomes one of your most valuable operational tools — not just a tax document.

Comparing your P&L month over month reveals seasonal patterns, identifies months where expenses spiked unexpectedly, and shows whether revenue growth is translating into improved profitability or simply higher costs. Comparing your current P&L to the same period in the prior year gives you a year-over-year performance view that removes seasonal noise.

If you’re considering hiring, expanding, or taking on a significant new expense, your P&L tells you whether your operating margin can absorb that cost without eliminating profitability. If a lender or investor asks for financial statements, your P&L is the primary document they’ll use to evaluate the earning power of your business. If you’re planning to sell the business someday, your P&L is a central driver of how a buyer will value it.

At Arizona Tax Accounting and Consulting Services, we consistently find that Phoenix business owners who review their P&L regularly — and understand what they’re reading — make better decisions, catch problems faster, and build more financially healthy businesses over time. The P&L is not just accounting paperwork. It’s one of the clearest windows into the true performance of everything you’ve built.

Conclusion

A Profit & Loss statement doesn’t have to be intimidating. Once you understand the flow — revenue at the top, direct costs subtracted to get gross profit, operating expenses subtracted to get operating income, and final adjustments to arrive at net profit — it becomes a document you can read, interpret, and act on with confidence. The eight numbers covered in this guide — revenue, COGS, gross profit, operating expenses, operating income, other income and expenses, interest and taxes, and net profit — tell the complete financial story of your business’s performance for any given period.

For Phoenix business owners, making the P&L a regular part of your monthly management routine is one of the highest-leverage habits you can build. It removes the guesswork from your financial decisions, gives you the data to have more productive conversations with your accountant, and ensures that the business you’ve worked hard to build is performing as well as you think it is — or reveals clearly where it needs attention before small problems become big ones.

If you’d like help setting up accurate financial statements, understanding what your P&L is telling you, or putting together a tax strategy built on real financial data, Arizona Tax Accounting and Consulting Services is here to help. Reach out to our Phoenix team today and take the guesswork out of your finances.