One of the most consequential decisions an Arizona business owner can make isn’t about marketing or operations — it’s about how their business is structured for tax purposes. The choice between operating as a standard LLC and electing S-Corporation status sounds like a question for accountants and attorneys, but the financial impact lands directly in your pocket. Done right, choosing the correct structure can save you thousands of dollars per year in self-employment taxes. Done wrong, it creates unnecessary complexity, compliance risk, and costs that eat into the savings you were hoping to capture.

This article breaks down exactly how LLCs and S-Corps work in Arizona, where the tax differences actually show up, what the real costs and obligations of each structure are, and how to determine which one makes more sense for your specific situation. The answer isn’t the same for every business owner, and anyone who tells you otherwise isn’t giving you the full picture.

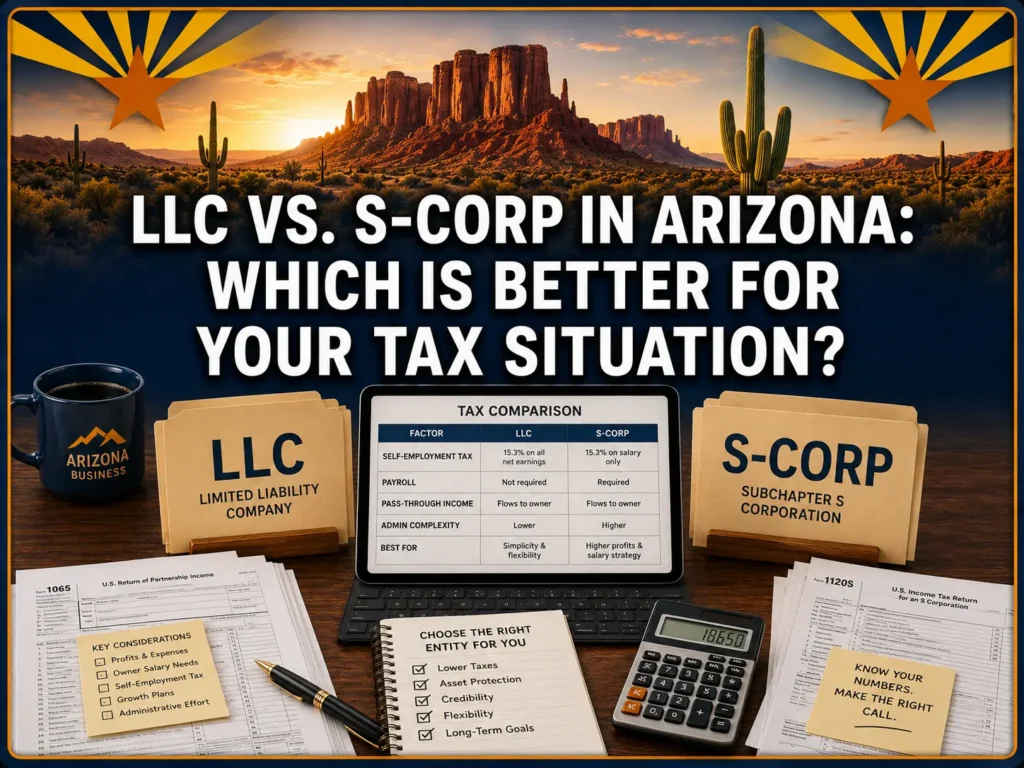

How Each Structure Works

The Standard LLC

A Limited Liability Company is the most common business structure chosen by Arizona small business owners, and for good reason. It provides personal liability protection — meaning your personal assets are generally shielded from business debts and legal claims — while keeping the administrative requirements relatively simple compared to a corporation.

From a federal tax perspective, a single-member LLC is treated as a “disregarded entity” by default, meaning the IRS ignores the LLC as a separate taxpayer and taxes the business income directly on the owner’s personal return via Schedule C. A multi-member LLC is taxed as a partnership by default, with income flowing through to each member’s personal return via Schedule K-1. In either case, the key tax reality is this: the IRS treats all net business income as self-employment income, which means the owner pays self-employment tax — currently 15.3% on the first $176,100 of net income and 2.9% above that threshold — on every dollar of profit the business generates.

That self-employment tax rate covers both the employee and employer portions of Social Security and Medicare. When you work for someone else, your employer pays half of this. When you’re self-employed, you cover both sides. For a business generating $150,000 in net profit, that’s roughly $21,000 in self-employment tax on top of your federal and Arizona income tax liability. This is the core financial problem that the S-Corp election is designed to address.

The S-Corporation

An S-Corporation is not a separate legal entity in the way most people imagine it. In Arizona, the vast majority of business owners who “elect S-Corp status” are simply taking their existing LLC and filing IRS Form 2553 to change how the federal government taxes that LLC. The LLC itself remains intact — same operating agreement, same liability protection, same state-level structure. What changes is the federal tax treatment.

Under S-Corp taxation, the business’s net profit is split into two components: a W-2 salary paid to the owner-operator and distributions of the remaining profit. The W-2 salary is subject to payroll taxes — the same Social Security and Medicare taxes that apply to any employee. The distributions, however, are not subject to self-employment tax or FICA. This is the source of the tax savings. By running a portion of your income through as a distribution rather than all of it through as self-employment income, you reduce the total dollars subject to the 15.3% self-employment tax rate.

A simple illustration makes this concrete. Assume your business earns $200,000 in net profit, and a reasonable salary for your role is $90,000. As a standard LLC, you pay self-employment tax on the full $200,000. As an S-Corp, you pay payroll taxes on $90,000 and take the remaining $110,000 as a distribution free of self-employment and FICA taxes. The tax savings on that $110,000 — roughly 15.3% — represent approximately $16,830 in reduced tax liability for the year, before accounting for the deductible half of self-employment tax and other adjustments.

The Reasonable Salary Requirement: The IRS’s Non-Negotiable Rule

The S-Corp tax strategy only works within a specific set of rules, and the most important one is the reasonable salary requirement. The IRS requires that any S-Corp shareholder who provides substantial services to the business must pay themselves a W-2 salary that reflects what the market would pay for that work. There is no specific number or percentage written into the tax code — it’s a facts-and-circumstances determination based on your industry, your experience, the time you spend in the business, and what comparable businesses pay for similar roles.

This rule exists precisely because the IRS knows about the self-employment tax split. The agency has consistently challenged S-Corp owners who pay themselves artificially low salaries to maximize the distribution portion. Courts have repeatedly sided with the IRS in these cases, and the penalty exposure includes back payroll taxes, interest, and significant penalties that can easily exceed the original tax savings. The so-called “60/40” split — paying yourself 60% as salary and taking 40% as distributions — is sometimes referenced as a guideline, but it has no legal standing and is not a safe harbor. Your salary needs to reflect the actual market value for your specific role.

Practically, setting a reasonable salary requires genuine research into what your position would command in the open market. A licensed electrician running a trade business, a marketing consultant, a software developer, and a dentist all have different labor market reference points. The stronger the documentation supporting your salary decision, the better your position if the IRS ever questions it.

The Real Costs of Operating as an S-Corp

The tax savings are real, but they don’t come free. The additional compliance obligations of S-Corp status carry both time and dollar costs that need to be factored into the decision before you elect.

Payroll

The moment you elect S-Corp status, you are required to run payroll and pay yourself a W-2 salary. This means setting up a payroll system, calculating and withholding federal income tax, Social Security, and Medicare from each paycheck, remitting those deposits to the IRS on a schedule that depends on your payroll size, filing quarterly payroll tax returns (Form 941), and filing annual payroll reconciliation returns (Form W-3 and W-2). In Arizona, you also have state income tax withholding obligations to the Arizona Department of Revenue. Payroll services like Gusto, ADP, or QuickBooks Payroll handle most of this mechanically, but they carry a monthly fee typically ranging from $40 to $100 per month, depending on the plan.

Tax Preparation

S-Corps file a separate federal tax return — Form 1120-S — in addition to your personal Form 1040. Arizona has a corresponding state S-Corp return. The cost of preparing business tax returns separately from your personal return is higher than filing a Schedule C as a sole proprietor or single-member LLC. Most CPA firms charge meaningfully more for S-Corp returns, which is a real and recurring annual cost.

Arizona-Specific Fees

Arizona does not impose a separate franchise tax or income tax at the entity level on S-Corps, which is an advantage compared to states like California that charge an $800 annual minimum franchise tax on S-Corps regardless of profitability. Arizona LLCs do have an annual report fee, and S-Corp status doesn’t eliminate the underlying LLC’s state obligations. The added compliance burden in Arizona is primarily federal in nature, not state, which makes the cost calculation somewhat more favorable here than in other states.

When the S-Corp Election Makes Financial Sense

The central question is straightforward: do the tax savings exceed the additional costs? The answer depends primarily on the net profit your business generates and what constitutes a reasonable salary for your role.

If your net profit is modest — say, below $40,000 to $50,000 per year — the S-Corp election typically doesn’t pencil out. The payroll setup costs, monthly payroll service fees, and higher tax preparation expenses can approach or exceed the self-employment tax savings at lower income levels. The math simply doesn’t work in your favor until the business is generating enough profit that there’s a meaningful spread between your reasonable salary and your total net income.

As net profit grows, the savings calculation shifts. At $100,000 in net profit with a $60,000 reasonable salary, the potential self-employment tax savings on the $40,000 distribution amount to roughly $6,120. That’s meaningful but needs to be weighed against total annual S-Corp administration costs that might run $2,000 to $3,500 when you factor in payroll services and additional tax preparation fees. The net benefit is positive but not dramatic.

At $150,000, $200,000, and beyond in net profit, the savings grow substantially, and the fixed administrative costs become a smaller percentage of the benefit. This is why experienced Arizona CPAs and tax advisors commonly suggest that the S-Corp election starts making real sense when your business consistently generates net profit that meaningfully exceeds a reasonable salary for your role — often cited as somewhere in the range of $80,000 to $100,000+ in net earnings, though the right threshold varies by industry and individual circumstances.

The Qualified Business Income Deduction Interaction

One often-overlooked factor in the LLC vs. S-Corp decision is how each structure interacts with the Section 199A Qualified Business Income (QBI) deduction, which allows eligible pass-through business owners to deduct up to 20% of qualified business income from their federal taxable income.

The QBI deduction is available to both standard LLCs and S-Corps. However, W-2 wages paid by the business are one of the limitation factors that determines the maximum QBI deduction amount at higher income levels. For S-Corp owners with income above the threshold amounts, the W-2 wages paid — including the owner’s salary — can actually increase the allowable QBI deduction. This adds another dimension to the salary-setting decision and reinforces why the LLC vs. S-Corp analysis should always involve a tax professional who can model the specific numbers for your situation rather than applying a generic rule of thumb.

Ownership and Eligibility Restrictions

If you’re considering the S-Corp election, it’s important to understand that S-Corporation status comes with eligibility restrictions that don’t apply to a standard LLC.

To qualify and maintain S-Corp status, your business must meet the following IRS requirements:

- No more than 100 shareholders total

- All shareholders must be U.S. citizens or permanent residents

- Only one class of stock is permitted — no preferred shares or classes with different economic rights

- Shareholders cannot be other corporations, partnerships, or most types of trusts

For most small Arizona business owners operating as a single-member LLC or a small partnership, these restrictions aren’t immediately limiting. But if you’re planning to bring in outside investment, add partners with complex ownership arrangements, or have any foreign national shareholders, the S-Corp election may create structural problems that a standard LLC would avoid. This is another area where getting professional input before electing is far better than discovering the constraint after the fact.

How to Make the S-Corp Election in Arizona

If the analysis points toward S-Corp status being the right move, the mechanical process involves filing IRS Form 2553 with the Internal Revenue Service. To have the election effective for the current tax year, the filing deadline is the 15th day of the third month of the tax year — for a calendar-year business, that’s March 15th. Filing after that date means the election takes effect in the following tax year unless you qualify for late election relief, which the IRS does grant under certain circumstances when the failure to file timely was due to reasonable cause.

You do not file a separate state form in Arizona to elect S-Corp status for state purposes — Arizona automatically recognizes the federal S-Corp election for state income tax purposes. However, you will need to ensure your business is registered with the Arizona Department of Revenue for employer withholding tax once you begin running payroll.

The timing of the election matters more than many business owners realize. Electing mid-year creates a partial-year situation where some income is taxed under the old structure and some under the new one. Planning the election for the beginning of a new tax year is cleaner and avoids the complexity of split-year reporting. For new businesses, the election can be made at formation if filed within the 75-day window.

Key Differences at a Glance

| Factor | Standard LLC | S-Corp Election |

| Self-employment tax | On all net profit | Only on W-2 salary |

| Payroll required | No | Yes |

| Tax return complexity | Schedule C or K-1 | Separate Form 1120-S |

| Annual admin cost | Lower | Higher |

| Ownership restrictions | Flexible | 100 shareholder limit, U.S. citizens only |

| Best income range | Under ~$80K net profit | Over ~$80K–$100K net profit |

| Arizona entity-level tax | No | No |

Conclusion

The LLC vs. S-Corp decision in Arizona is fundamentally a math problem layered on top of a compliance reality. The tax savings from S-Corp status are genuine and can be substantial — but they only materialize when your net profit is high enough to justify the additional payroll, accounting, and administrative costs that come with the structure. Below a certain income threshold, the standard LLC is the simpler and more cost-effective choice. Above that threshold, the S-Corp election can put thousands of dollars back in your pocket every year.

What makes this decision genuinely complex is the number of individual variables involved — your specific net profit level, what constitutes a reasonable salary in your industry, how the QBI deduction interacts with your income, your business growth trajectory, and whether ownership restrictions create any structural concerns. These factors combine differently for every business owner, which is why a one-size-fits-all answer doesn’t exist.

At Arizona Tax Accounting and Consulting Services, our team works with Arizona business owners to model the actual numbers for their specific situation — not just explain the concepts, but calculate the real-world tax impact so you can make a decision based on facts rather than assumptions. Whether you’re evaluating the S-Corp election for the first time or wondering whether your current structure is still the right fit as your income grows, we’re here to help you get it right. Reach out today and put the right tax strategy to work for your business.